You have to really question what passes for financial analysis these days. One financial show was discussing the recent increase in consumer debt as something positive. In the same breath this person also said that households increased savings. Now think about this statement. If you financed a $2,000 vacation on your credit card but increased savings by $500 did your balance sheet improve? Of course not. Let us not even dive into the fact that most of the recent consumer debt increase has come at the hands of student debt which is already in a massive bubble. We are simply repeating the same mistakes with a different soundtrack. We are trying to get out of a debt led crisis with more debt. The facts even show this and we have compiled some of the more troubling data by putting the entire debt market into perspective here. Is it really possible to solve a problem based on too much debt with more debt?

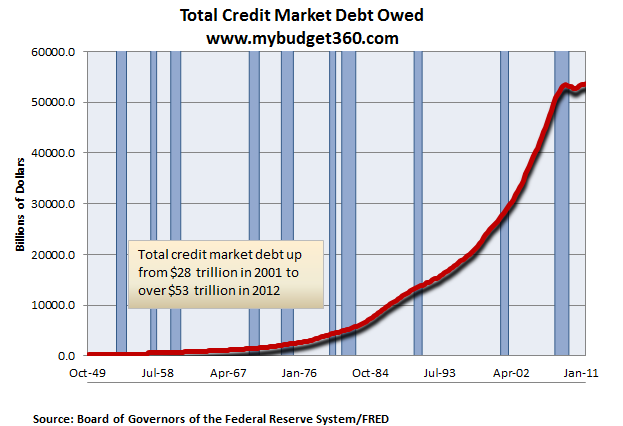

The total market of debt shows our addiction to borrowed money

We flat out have an addiction to borrowing. Total market debt is now up to an astonishing $53 trillion and continues to grow. Take a look at this frightening data:

In 2001 total credit market debt was up to $28 trillion. Today it is now well above $53 trillion and inching closer to slapping on another trillion dollars this year. If you look at Greece as a microcosm of the bigger issue, you realize they are treating a solvency issue as if it were a liquidity issue. Let us be absolutely clear that all of this debt will never be paid off. This warrants repeating:

“The $53 trillion in total credit market debt will never be fully repaid.”

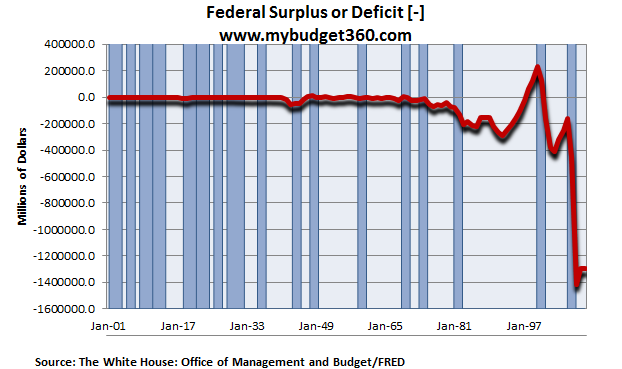

In essence the total debt markets are growing even though the debt will never be paid off. Since most thinking people get this, the banking sector is leveraging central banks to basically print money since no person would lend money out knowing they would never be paid back. Do people really think we are going to pay off our $15 trillion national debt when our deficits look like this:

We’ve been running continuous budget deficits since the late 1970s. We had a brief respite when it came to having a surplus with the tech boom but that was blown out the window completely with the real estate mania. Contrary to what most will say, deficits do matter and massive deficits really matter.

Let us be abundantly clear that the total market debt is incredible. You now start having this challenging race where you are trying to avoid having your total debt surpass your annual GDP. The US has passed that mark and so have many other countries. The results in the long-run are never positive especially when people wise up and start asking for their money back. Since most don’t have the funds, they pay for it via inflation and a devaluation of their currencies. A few articles have circulated where Greece is trying to enforce stronger tax collections yet their system on collecting taxes is so corrupted that they have no way of achieving this without completely revamping the system.

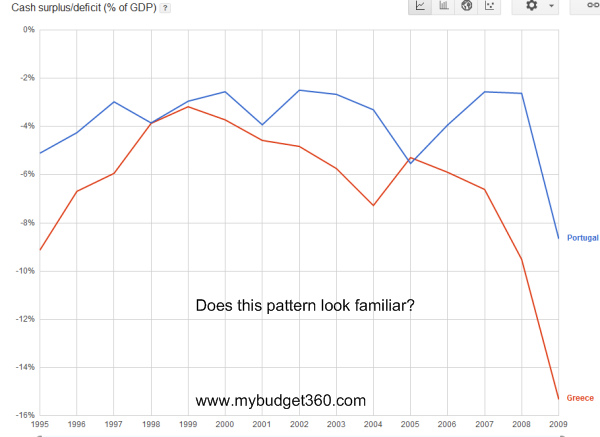

If you think Europe is done just look at Portugal since they are next in the debt grinder queue:

To the debt increase in the US

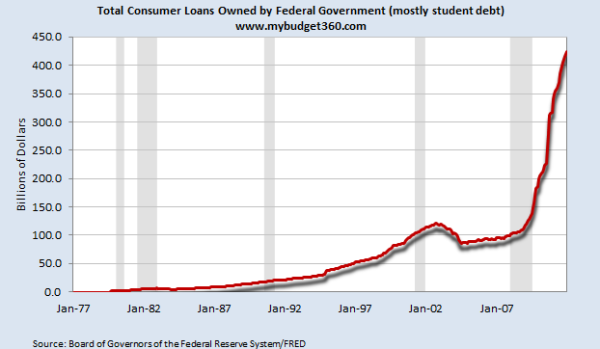

The access to easy debt creates massive amounts of bubbles. We saw this in housing and now we are seeing it here in the US with the giant higher education bubble:

Keep in mind this is only a tiny part of the student debt market. This year we will surpass $1 trillion point for student loan debt. I believe this will be another crisis that will hit and many indebted students are already feeling this. Many are being sucked into paper mill for-profits that are essentially scam factories that raid the government backed student loan funds. They lobby Congress to make it easier for them to report horrific placement data and change the metric on default reporting so it doesn’t look as atrocious. Even with these softballs from our bought out politicians, the data is still horrible.

A debt bubble cannot be solved with more debt. That should be obvious just like saying savings increased but people went into more debt should cause you to pause. Yet few in the financial media ever take a timeout and many missed the tech bubble bust, the housing bubble bust, and gear up because they will miss the other debt bubble bust as well.

“Is the “fiscal cliff” real or just another hoax? The answer is that the fiscal cliff is real, but it is a result, not a cause. The hoax is the way the fiscal cliff is being used.”

-x-x-x-x-x-x-x-x-x-

December 1, 2012

The fiscal cliff is the result of the inability to close the federal budget deficit. The budget deficit cannot be closed because large numbers of US middle class jobs and the GDP and tax base associated with them have been moved offshore, thus reducing federal revenues. The fiscal cliff cannot be closed because of the unfunded liabilities of eleven years of US-initiated wars against a half dozen Muslim countries–wars that have benefitted only the profits of the military/security complex and the territorial ambitions of Israel. The budget deficit cannot be closed, because economic policy is focused only on saving banks that wrongful financial deregulation allowed to speculate, to merge, and to become too big to fail, thus requiring public subsidies that vastly dwarf the totality of US welfare spending.

The hoax is the propaganda that the fiscal cliff can be avoided by reneging on promised Social Security and Medicare benefits that people have paid for with the payroll tax and by cutting back all aspects of the social safety net from food stamps to unemployment benefits to Medicaid, to housing subsidies. The right-wing has been trying to get rid of the social safety net ever since Franklin D. Roosevelt constructed it, out of fear or compassion or both, during the Great Depression.

Washington’s response to the fiscal cliff is austerity: spending cuts and tax increases. The Republicans say they will vote for the Democrats’ tax increases if the Democrats vote for the Republican’s assault on the social safety net. What bipartisan compromise means is a double-barreled dose of austerity.

Ever since John Maynard Keynes, economists have understood that tax increases and spending cuts suppress, not stimulate, economic activity. This is especially the case in an economy such as the American one, which is driven by consumer spending. When spending declines, so does the economy. When the economy declines, the budget deficit rises.

This is especially the case when an economy is weak and already in decline. A declining economy means less sales, less employment, less tax revenues. This works against the effort to close the federal budget deficit with austerity measures. Instead of strengthening the economy, the austerity measures weaken it further. To cut unemployment benefits and food stamps when unemployment is high or rising would be to provoke social and political instability.

Bread Lines of the Modern Era– The Great Recession IF all EBT recipients shopped at only Walmart Super Centers for ALL their SNAP benefits, then this is how the Bread Line would look each month– 14,588 people. There are 3051 Walmart Super Centers in USA and 44,510,598 participants in SNAP (2011), making the average SNAP line at each Walmart at 14,588 people. The Modern Era’s Bread Lines are not visible because the business is handled discreetly through EBT Cards. According to this Food Stamps report pg 16-17, Walmart receives half of all SNAP dollars in Oklahoma. Walmart is the largest retailer in America. Short Facts: 47% of Food Stamp participants are children. 78.6% of all SNAP participants are in metropolitan areas. 93.2% of all SNAP benefits go to US citizens. Only 4% are self-employed. (CLICK IMAGE FOR SOURCEPAGE)

Some economists, such as Robert Barro at Harvard University, claim that stimulative measures, the opposite of austerity, don’t work, because consumers anticipate the higher taxes that will be needed to cover the budget deficit and, therefore, reduce their spending and increase their saving in order to be able to pay the anticipated higher taxes.

In other words, the Keynesian effort to stimulate spending causes consumers to reduce their spending. I don’t know of any empirical evidence for this claim.

Regardless, the situation on the ground at the present time is that for the majority of people, incomes are stretched to the limit and beyond. Many cannot pay their bills, their mortgages, their car payments, their student loans. They are drowning in debt, and there is nothing that they can cut back in order to save money with which to pay higher taxes.

Many commentators are complaining that Congress will refuse to face the difficult issues and kick the can down the road, leaving the fiscal cliff looming. This would probably be the best outcome. As the fiscal cliff is a result, not a cause, to focus on the fiscal cliff is to focus on the symptoms rather than the disease.

The US economy has two serious diseases, and neither one is too much welfare spending.

One disease is the offshoring of US middle class jobs, both manufacturing jobs and professional service jobs such as engineering, research, design, and information technology, jobs that formerly were filled by US university graduates, but which today are sent abroad or are filled by foreigners brought in on H-1B work visas at two-thirds of the salary.

The other disease is the deregulation, especially the financial deregulation, that caused the ongoing financial crisis and created banks too big to fail, which has prevented capitalism from working and closing down insolvent corporations.

The Federal Reserve’s policy is focused on saving the banks, not on saving the economy. The Federal Reserve is purchasing not only new Treasury bonds issued to finance the more than one trillion dollar annual federal deficit but also the banks’ underwater financial instruments, taking them off the banks’ books and putting them on the Federal Reserve’s books.

Normally, debt monetization of this amount results in rising inflation, but the money that the Federal Reserve is creating in its attempt to manage the public debt and the banks’ private debt is hung up in the banking system as excess reserves and is not finding its way into the economy. The banks are too busted to lend, and consumers are too indebted to borrow.

However, the debt monetization poses a second threat that is capable of biting the US economy and consumer living standards very hard. Foreign central banks, foreign investors in US stocks and financial instruments, and Americans themselves observing the Federal Reserve’s continuous monetization of US debt cannot avoid concern about the dollar’s value as the supply of ever more dollars continues to pour out of the Federal Reserve.

Already there is evidence of central banks and individuals moving out of dollars into gold and silver bullion and into other currencies of countries that are not hemorrhaging debt and money. According to John Williams of Shadowstats.com, the US dollar as a percentage of global holdings of reserve assets has declined from 36.6% in 2006 to 28.7% in 2012. Gold has increased from 10.5% to 12.8% and other foreign currencies except the euro increased from 38.4% to 44.4%.

Russia, China, Brazil, India, and South Africa intend to conduct trade among themselves in their own currencies without use of the dollar as reserve currency. The EU countries conduct their trade with one another in euros, and although not reported in the US media, Asian countries are discussing a new common currency for trade among themselves.

The world is abandoning the use of the dollar to settle international accounts, and the demand for dollars is falling as the Federal Reserve increases the supply of dollars.

This means that the price of the dollar is threatened.

Concern over the dollar means concern over dollar-denominated financial instruments such as stocks and bonds. The Chinese hold some $2 trillion in US financial instruments. The Japanese hold about $1 trillion in US Treasuries. The Saudis and the oil emirates also hold large quantities of US dollar financial instruments. At some point the move away from the dollar also means a move away from US financial instruments. The dumping of US stocks and bonds would destabilize US financial markets and wipe out the remainder of US wealth.

As I have previously written, the Federal Reserve can create new money with which to purchase the dumped financial instruments, thus maintaining their prices. But the Federal Reserve cannot print gold or foreign currencies with which to buy up the dollars that foreigners are paid for their US stocks and bonds. When the dollars in turn are dumped, the exchange value of the dollar will collapse, and US inflation will explode.

The onset of hyperinflation can be as sudden as the collapse of a currency’s exchange value.

The real crisis facing the US is the impending collapse of the US dollar’s foreign exchange value. The US dollar’s value in relation to silver and gold has already collapsed. In the past ten years, gold’s price in US dollars has increased from $250 per ounce to $1,750 per ounce, an increase of $1,500. Silver’s price has risen from $4 per ounce to $34 per ounce. These price rises are not due to a sudden scarcity of gold and silver, but to a flight from the dollar into the two forms of historical money that cannot be created with the printing press.

The price of oil has risen from $20 a barrel ten years ago to as high as $120 per barrel earlier this year and currently $90 a barrel. This price rise has come about despite a weak world economy and without any supply restrictions other than those caused by the attempted US occupation of Iraq, the Western assault on Libya, and the self-harming Western sanctions on Iran, impacts most likely offset by the Saudis, still Washington’s faithful puppet, a country that pumps out its precious life fluid in order to save the West from its own mistakes. The moronic neoconservatives wish to overthrow the Saudi Arabian government, but what more faithful servant has Washington ever had than the Saudi royal house?

What can be done? For a number of years I have pointed out that the problem is the loss of US employment, consumer income, GDP, and tax base to offshoring. The solution is to reverse the outward flow of jobs and to bring them back to the US. This can be done, as Ralph Gomory has made clear, by taxing corporations according to where they add value to their product. If the value is added abroad, corporations would have a high tax rate. If they add value domestically with US labor, they would face a low tax rate. The difference in tax rates can be calculated to offset the benefit of the lower cost of foreign labor.

As all offshored production that is brought to the US to be marketed to Americans counts as imports, relocating the production in the US would decrease the trade deficit, thus strengthening belief in the dollar. The increase in US consumer incomes would raise tax revenues, thus lowering the budget deficit. It is a win-win solution.

The second part to the solution is to end the expensive unfunded wars that have ruined the federal budget for the past 11 years as well as future budgets due to the cost of veterans’ hospital care and benefits. According to ABC World News, “In the decade since the Sept. 11, 2001 terrorist attacks on the World Trade Center, 2,333,972 American military personnel have been deployed to Iraq, Afghanistan or both, as of Aug. 30, 2011 [more than a year ago].” These 2.3 million veterans have rights to various unfunded benefits including life-long health care. Already, according to ABC, 711,986 have used Veterans Administration health care between fiscal year 2002 and the third-quarter of fiscal year 2011. http://abcnews.go.com/Politics/us-veterans-numbers/story?id=14928136#1

The Republicans are determined to continue the gratuitous wars and to make the 99 percent pay for the neoconservatives’ Wars of Hegemony while protecting the 1 percent from tax increases.

The Democrats are little different.

No one in the White House and no more than one dozen members of the 535 member US Congress represents the American people. This is the reason that despite obvious remedies nothing can be done. America is going to crash big time.

And the rest of the world will be thankful. America along with Israel is the world’s most hated country. Don’t expect any foreign bailouts of the failed “superpower.”

SPOILER: DO-NOT-FALL-FOR-THAT!! This all-coming ‘goldrush’ is artificially supported in order to actually KEEP the US Dollar’s status-quo in tradings – that is, until it finally collapses.

I repeat: BEWARE. Do not fall for that trick, as it’s what banks would like the most. That’s exactly why they pay people like this to write essays like these.

I warned ye.

-x-x-x-x-x-x-x-x-x-

Marc Howe | November 30, 2012

On the eve of the implementation of the Basel III capital rules governing the world’s largest financial institutions veteran investor Eric Sprott points to gold as the most convenient and over-looked solution to the global banking system’s woes.

The Basel Committee on Banking Supervision, responsible for devising guidelines for the world’s leading financial institutions, has spent the past four years since the Great Financial Crisis drafting a new set of international banking regulations to prevent the recurrence of similar catastrophes.

The new rules are slated to take effect on 1 January 2013, yet only months prior to their scheduled implementation they have already triggered refractory responses – particularly in the United States, due to their complexity and adverse impact on profits.

In a trenchant essay on the new regulations Sprott highlights what he believes to be one of their chief defects – their treatment of gold as an asset class.

Sprott notes that Basel III regulators cling to the notion that AAA-government securities should comprise the preponderance of high quality liquid assets which banks are required to hold.

Such securities are no longer esteemed by the financial community as safe harbor holdings due to the sovereign risk issues blighting a number of indebted nation-states, as well as the propensity of governments to issue blithely issue debt.

According to Sprott, precious metals such as gold could be the solution to the instability of the global banking system were they conferred with a heightened liquidity profile under the new Basel III framework.

Sprott writes that this would “open the door for gold to compete with cash and government bonds on bank balance sheets – and provide banks with an asset that actually has the chance to appreciate.”

Non-Western central banks have already cottoned on to this and included gold as a key component of their foreign exchange reserves, while two banking jurisdictions in particular – Turkey and China – “have openly incorporated gold into their capital structures.”

The People’s Bank of China recently made remarks which would imply that the government wishes to capitalize on their growing gold stockpile by integrating the domestic market with the international market, and Sprott speculates that China “may have already cornered most of the world’s physical gold supply” in anticipation of the day that Western banks realize that the precious metal is preferable to Treasuries.

Hiding behind the complexities of our financial system, banks and other institutions are being accused of fraud and deception, with Goldman Sachs just the latest in the spotlight. This has become the most pressing election issue of all

Goldman Sachs was in the spotlight last November when demonstrators protested outside its Washington offices against executive bonuses. Photograph: Andrew Harrer/Bloomberg via Getty Images (click images for their sourcepages)

Will Hutton

The Observer, Sunday 18 April 2010

The global financial crisis, it is now clear, was caused not just by the bankers’ colossal mismanagement. No, it was due also to the new financial complexity offering up the opportunity for widespread, systemic fraud. Friday’s announcement that the world’s most famous investment bank, Goldman Sachs, is to face civil charges for fraud brought by the American regulator is but the latest of a series of investigations that have been launched, arrests made and charges made against financial institutions around the world. Big Finance in the 21st century turns out to have been Big Fraud. Yet Britain, centre of the world financial system, has not yet levelled charges against any bank; all that we’ve seen is the allegation of a high-level insider dealing ring which, embarrassingly, involves a banker advising the government. We have to live with the fiction that our banks and bankers are whiter than white, and any attempt to investigate them and their institutions will lead to a mass exodus to the mountains of Switzerland. The politicians of the Labour and Tory party alike are Bambis amid the wolves.

Just consider the roll call beyond Goldman Sachs. In Ireland Sean FitzPatrick, the ex-chair of the Anglo Irish bank was arrested last month and questioned over alleged fraud. In Iceland last week a dossier assembled by its parliament on the Icelandic banks – huge lenders in Britain – was handed to its public prosecution service. A court-appointed examiner found that collapsed investment bank Lehman knowingly manipulated its balance sheet to make it look stronger than it was – accounts originally audited by the British firm Ernst and Young and given the legal green light by the British firm Linklaters. In Switzerland UBS has been defending itself from the US’s Internal Revenue Service for allegedly running 17,000 offshore accounts to evade tax. Be sure there are more revelations to come – except in saintly Britain.

The shape of CDOs to come (Cayman Financial Review)

Beneath the complexity, the charges are all rooted in the same phenomenon – deception. Somebody, somewhere, was knowingly fooled by banks and bankers – sometimes governments over tax, sometimes regulators and investors over the probity of balance sheets and profits and sometimes, as the Securities and Exchange Commission (SEC) says in Goldman’s case, by creating a scheme to enrich one favoured investor at the expense of others – including, via RBS, the British taxpayer. Along the way there is a long list of so-called “entrepreneurs” and “innovators” who were offered loans that should never have been made. Lloyd Blankfein, Goldman’s CEO, remarked only semi-ironically that his bank was doing God’s work. He must wake up every day bitterly regretting the words ever emerged from his mouth.

For the Goldmans case is in some ways the most damaging. The Icelandic banks, Anglo Irish bank and Lehman were all involved in opaque deals and rank bad lending decisions – but Goldman allegedly went one step further, according to the SEC actively creating a financial instrument that transferred wealth to one favoured client from others less favoured. If the Securities and Exchange Commission’s case is proved – and it is aggressively rebutted by Goldman – the charge is that Goldman’s vice-president Fabrice Tourre created a dud financial instrument packed with valueless sub- prime mortgages at the instruction of hedge fund client Paulson, sold it to investors knowing it was valueless, and then allowed Paulson to profit from the dud financial instrument. Goldman says the buyers were “among the most sophisticated mortgage investors” in the world. But this is a used car salesman flogging a broken car he’s got from some wide-boy pal to some driver who can’t get access to the log-book. Except it was lionised as financial innovation.

Banks in talks to end bond probe (Wallstreet Journal)

The investors who bought the collateralised debt obligation (CDO) were not complete innocents. They had asked for the bond to be validated by an independent expert into residential mortgage-backed securities – a company called ACA management. ACA gave the bond the thumbs-up on the understanding from Fabrice Tourre that the hedge fund Paulson were investing in it. But the SEC says Tourre misled them, a pivotal claim that Goldman denies. The reality was that Paulson was frantically buying credit default swaps in the CDO that would go up in price the more valueless it became – a trade that would make more than $1 billion. Worse, Paulson had identified some of the dud sub-prime mortgages that he wanted Tourre to put into the CDO. If the SEC case is true, this was a scam – nothing more, nothing less.

Tourre could see what was coming. In one email in January 2007 he wrote: “More and more leverage in the system. The whole building is about to collapse anytime now… only potential survivor, the fabulous Fab[rice Tourre] .. standing in the middle of all these complex highly leveraged exotic trades he created without necessarily understanding all of the implications of those monstrosities”. Fabulous Fab, like his boss, will not be feeling very fab today.

Hedging their bets — about exactly WHO owns your Mortgage? (Daily KOS)

The cases not only have a lot in common – using financial complexity allegedly to deceive and then using so-called independent experts to validate the deception (lawyers, accountants, credit rating agencies, “portfolio selection agents,” etc etc ) – but they also show how interconnected the financial system is. In Iceland Citigroup and Deutsche Bank covered the margin calls of distressed Icelandic business borrowers, deepening the crisis. Lehman uses the lightly regulated London markets and two independent British experts to validate that their “Repo 105s” were “genuine” trades and not their own in-house liability. The American authorities pursued a Swiss bank over aiding and abetting US nationals to evade tax.

Hedging their bets — about exactly WHO owns your Mortgage? (Daily KOS)

Bankers will complain these cases all involve one or two misguided individuals, but that most banking is above board and was just the victim of irrational exuberance, misguided belief in free market economics and faulty risk management techniques. Obviously that is true – but, sadly, there is much more to the crisis. Andrew Haldane, executive director of the Bank of England, highlights the remarkable reduction in the risk weighting of bank assets between 1997 and 2007. Put simply, Europe’s and the US’s large banks exploited the weak international agreement on bank capital requirements in the so-called Basel agreement in 2004 to reclassify the risk of their loans and trading instruments. They did not just reduce the risk by 5 or 10%. Breathtakingly, they claimed their new risk management techniques were so wonderful that the riskiness of their assets was up to half of what it had been – despite property and share prices cresting to new all-time highs.

Brutally, the banks knowingly gamed the system to grow their balance sheets ever faster and with even less capital underpinning them in the full knowledge that everything rested on the bogus claim that their lending was now much less risky. That was not all they were doing. As Michael Lewis describes in The Big Short, credit default swaps had been deliberately created as an asset class by the big investment banks to allow hedge funds to speculate against collateralised debt obligations. The banks were gaming the regulators and investors alike – and they knew full well what they were doing. Simon Johnson’s 13 Bankers shows how the major American banks deployed vast political lobbying power and money to create the relaxed regulatory environment in which all this could take place. In Britain no money changed hands. Gordon Brown offered light-touch regulation for free – egged on by the Tories, who wanted to go further.

CDOs for Dummies (The Big Picture)

This was the context in which Goldman’s Fabulous Fab created the disputed CDOs, Sean FitzPatrick allegedly moved loans between banks and Lehman created its Repo 105s along with the entire “debt mule” structure revealed this weekend of inter-related companies to shuffle debt around its empire. London and New York had become the centre of an international financial system in which the purpose of banking became making money from money – and where the complexity of the “innovations” allowed extensive fraud and deception.

Now it has all collapsed, to be bailed out by western taxpayers. The banks are resisting reform – and want to cling on to the business practices and business model that has so appallingly failed. It is obvious why: it makes them very rich. The politicians tread carefully, only proposing what the bankers say is congruent with their definition of what banking should be. Labour and Tories alike are united in opposing improved EU regulation of hedge funds, buying the propaganda those operations had nothing to do with the crisis. Perhaps Paulson’s trades at Goldman, and the hedge funds’ appetite for speculating in credit default swaps, may disabuse them.

Goldman Sachs has a derivative exposure of $44.192 Trillion dollars. The $1 Trillion pillars towers are double-stacked @ 930 feet (248 m). The White House is standing next to the Statue of Liberty. Goldman Sachs has advantage over other banks because it has awesome connections in US Government. A lot of former Goldman employees hold high-level US Government positions (chart). Mitt Romney’s top donor is Goldman Sachs, and one of Obama’s best donors. Ex-CEO of Goldman Sachs, Hank Paulson became the Secretary of Treasury under Bush and during the 2008 financial crisis authored the TARP bill demanding $700 billion bail-out. In UK, Goldman Sachs escaped £10 million bill on a failed tax avoidance scheme with help of good connections. The bank is the largest player in the food commodities market, earned $955m from food speculation in 2009″ – That’s your $$$. Goldman Sachs employees are arming themselves with guns in case there is a populist uprising against the bank. Goldman Sachs calls their investors “muppets”. and use clients to make money for themselves, disregarding the clients. The bank was fined $22 million for sharing valuable nonpublic information with top clients (Think insider trading with best clients). Goldman Sachs was part-owner America’s leading website for prostitution ads until the ownership stake was exposed. Goldman Sachs helped Greece conceal its debt with secret loans, while simultaneously taking advantage of Greece. Goldman Sachs got a $814 billion SECRET bailout from the Federal Reserve during the 2008 crisis. Goldman Sachs got $10 billion of the 2008 TARP bailout, and in the same year paid $10.9 billion in employee compensation and “benefits”, while paying a tax rate of 1%. That means an average of $327,000 to each Goldman Sach’s employee.

It is time to reframe the question. Banks and financial institutions should do what economy and society want them to do – support enterprise, direct credit to where it is needed and be part of the system that generates investment and innovation. Andrew Haldane – and the governor of the Bank of England – are right. We need to break up our banks, limit their capacity to speculate and bring them back to earth. Britain should also launch an official investigation into what went wrong – and hand the findings to the Serious Fraud Office. This needs to become this election campaign’s number one issue – not one which either a compromised Labour party or a temporising Conservative party will relish. The Lib Dems, the fiercest critics of the banks, have begun to get very lucky.

By Nicholas Larkin and Debarati Roy – Nov 20, 2012 7:39 PM GMT-0200

Gold’s 12-year rally, the longest in at least nine decades, is poised to continue in 2013 as central bank stimulus spurs investors from John Paulson to George Soros to accumulate the highest combined bullion holdings ever.

Bank of England’s glittering stash of £156 BILLION in gold bars stored in former canteen under London. (click image for sourcepage)

The metal will rise every quarter next year and average $1,925 an ounce in the final three months, or 11 percent more than now, according to the median of 16 analyst estimates compiled by Bloomberg. Paulson & Co. has a $3.66 billion bet through the SPDR Gold Trust, the biggest gold-backed exchange- traded product, and Soros Fund Management LLC increased its holdings by 49 percent in the third quarter, U.S. Securities and Exchange Commission filings show.

Central banks from Europe to China are pledging more steps to boost growth, raising concern about inflation and currency devaluation. Investors bought 247.5 metric tons through ETPs this year, exceeding annual U.S. mine output. While both sides said talks Nov. 16 between President Barack Obama and Congress over the so-called fiscal cliff were “constructive,” the Congressional Budget Office has warned the U.S. risks a recession if spending cuts and tax rises aren’t resolved.

“We see gold as a hedge against the follies of politicians,” said Michael Mullaney, who helps manage $9.5 billion of assets as chief investment officer at Fiduciary Trust in Boston. “It’s a good time to garner some protection in portfolios by having some real asset like gold.”

Longest Streak

Gold advanced 11 percent to $1,728.85 in London this year, headed for a 12th consecutive annual gain, the longest streak in data compiled by Bloomberg going back to 1920. Prices reached a record $1,921.15 in September 2011. The Standard & Poor’s GSCI gauge of 24 commodities slipped 0.3 percent and the MSCI All- Country World Index (MXWD) of equities climbed 8.2 percent. Treasuries returned 2.7 percent, a Bank of America Corp. index shows.

Bullion held through ETPs, the first of which listed in 2003, reached a record 2,604.2 tons yesterday, valued at $144.9 billion. That exceeds the official reserves of every nation except the U.S. and Germany, World Gold Council data show. The SPDR Gold Trust (GLD) alone holds 1,342.2 tons.

Global Teutonic Zionists – Working towards that New World Order: 1) Lord Jacob de Rothschild. 2) His spooky son, Nathaniel. 3) Baron John de Rothschild, who recently said they are working towards global governance. 4) Sir Evelyn de Rothschild. His wife Lynn Forrester is a big mover and shaker in the Democratic party. 5) David Rockefeller, Sephardic Crypto-Teutonic, who’s son Nick told film director Aaron Russo about 9/11 in advance. 6) Nathan Warburg. His family was not only instrumental in creating the Federal Reserve, etc. they were also behind the rise of Adolf Hitler. 7) Henry Kissinger, Globalist genocidal schemer. 8 George Soros, another Teutonic schemer and NGO manipulator. 9) Paul Volcker, Crypto-Jew big-time Globalist and economic advisor to Obama. 10) Larry Summers, Crypto-Teutonic economic advisor to Obama. 11) Lloyd Blankfein, CEO to the rapidly growing Goldman Sachs banking behemoth. 12) Ben Shalom Bernanke, current Teutonic master of the Federal Reserve (a private entity, neither “Federal” nor a “Reserve”). What’s the common denominator here? (click image for sourcepage – ’tis a nice political blog, albeit somewhat homophobic, in my opinion. Nothing is perfect, after all…)

Soros increased his investment in the trust to 1.32 million shares in the third quarter, the most since 2010, a Nov. 14 SEC filing showed. The stake, with each share representing about a 10th of an ounce, is valued at $221.4 million. Prices advanced 60 percent since January 2010, when Soros called gold the “ultimate asset bubble.” Michael Vachon, a spokesman for the 82-year-old who made $1 billion breaking the Bank of England’s defense of the pound in 1992, declined to comment.

Official Reserves

Paulson, who became a billionaire in 2007 by wagering against the subprime mortgage market, owns 21.8 million shares in the SPDR Gold Trust, making him the biggest shareholder, a Nov. 15 SEC filing showed. The 56-year-old raised his stake by 26 percent in the second quarter and his holding of about 66 tons exceeds the official reserves of nations from Brazil to Bulgaria to Bolivia.

The New York-based hedge fund company reduced its investments in Anglogold Ashanti Ltd. (ANG) and Gold Fields Ltd., the third- and fourth-biggest producers. Armel Leslie of Walek & Associates, a spokesman for Paulson’s fund, declined to comment.

Paul Touradji’s Touradji Capital Management LP sold all of its 82,000 shares in the SPDR Gold Trust in the third quarter, according to an SEC filing. Lone Pine Capital LLC, the hedge fund run by Stephen Mandel Jr., cut its stake by 31 percent to 2.6 million shares, and Dan Loeb’s Third Point LLC lowered its bet by 10 percent to 130,000 shares, filings showed last week. Officials from all three companies declined to comment.

Nine Strategists

While some investors expect stimulus to devalue currencies, the median of nine strategist estimates compiled by Bloomberg show the U.S. Dollar Index, a measure against six major trading partners, will average 82.8 next year, from 80.9 now. Steven Englander, Citigroup Inc.’s head of G-10 strategy, said in an interview this month that the currency market is signaling it isn’t yet convinced the Federal Reserve will fulfill its pledge to pump record amounts of cash into the economy through 2015.

Third-quarter demand for gold fell 11 percent, the most since 2009, as China’s slowing growth curbed purchases, the London-based World Gold Council said Nov. 15. India, the biggest buyer in the quarter, consumed 24 percent less in the year’s first nine months as bullion priced in rupees reached a record in September. The Washington-based International Monetary Fund cut its 2013 forecast for world growth twice since July, to 3.6 percent.

Inflation Adjusted

While prices rose 25 percent since November 2010, the size of the futures market, based on contracts outstanding, fell 30 percent, bourse data show. The metal, down 3.7 percent from this year’s high, has yet to exceed previous records when adjusted for inflation, with its 1980 record of $850 equal to $2,398 today, data compiled by the Fed Bank of Minneapolis show.

Hedge funds and other large speculators pared bets on a rally in futures traded on the Comex bourse in New York by 29 percent since Oct. 9, U.S. Commodity Futures Trading Commission data show. They’re still holding a net-long position of 140,162 futures and options, about 10 percent more than this year’s average, and increased wagers by 7.7 percent last week.

The Fed said Oct. 24 it will maintain $40 billion in monthly purchases of mortgage debt and probably hold interest rates near zero until mid-2015. The European Central Bank said it’s ready to buy bonds of indebted nations and the Bank of Japan raised its asset-purchase program for the second time in two months on Oct. 30.

Quantitative Easing

Gold rallied 70 percent as the Fed bought $2.3 trillion of debt in two rounds of quantitative easing from December 2008 through June 2011.

Investors buying bullion as a hedge against inflation and a weaker dollar generally earn returns only through price gains, increasing its allure as interest rates decline. It rose sixfold since the end of 2000, beating the 34 percent advance in the S&P 500, with dividends reinvested, and the 91 percent return on Treasuries. The Dollar Index fell 26 percent.

The first face-to-face meeting between Obama and leaders from Congress on the fiscal cliff yielded optimism and few details about how it would be resolved. The $607 billion of automatic spending cuts and tax increases is scheduled to take effect in January. U.S. equities and Treasuries rose Nov. 16 and gold futures were little changed.

Options Trading

Credit Suisse Group AG’s Tom Kendall, the most accurate gold forecaster tracked by Bloomberg over the past two years, sees prices averaging $1,880 in the fourth quarter next year and UniCredit SpA’s Jochen Hitzfeld, ranked second, expects $1,950. Deutsche Bank AG’s Daniel Brebner, the next most accurate, predicts $2,300 in the third quarter.

Options traders are also bullish, with the seven most widely held contracts conferring the right to buy at prices from $1,800 to $2,200 between November and March, Comex data show.

Central banks added to reserves for 19 consecutive months through August, the longest streak since 1964, IMF data show. Nations from Russia to South Korea to Mexico bought more to bring combined holdings to 31,461 tons, equal to about 18 percent of all the metal ever mined.

Barrick Gold Corp. (ABX), the world’s largest producer, will report a 41 percent gain in profit to a record $5.04 billion next year, the mean of 10 analyst estimates compiled by Bloomberg shows. The Toronto-based company’s shares fell 25 percent this year and will gain 43 percent in the next 12 months, according to the average of 23 forecasts.

Monetary Stimulus

Analysts predict Newmont Mining Corp. (NEM) and AngloGold Ashanti, the next-biggest, will also report the most profit ever next year.

“It looks as though global monetary stimulus is likely to continue, particularly in the wake of growing fiscal austerity,” said Alan Gayle, a senior strategist at RidgeWorth Capital Management in Richmond, Virginia, which oversees about $47 billion of assets. “That puts pressure on the monetary authorities to stimulate the economy and that will debase the currencies and put a bid under gold.”

To contact the reporters on this story: Nicholas Larkin in London at nlarkin1@bloomberg.net; Debarati Roy in New York at droy5@bloomberg.net

To contact the editor responsible for this story: Steve Stroth at sstroth@bloomberg.net

Over the coming weeks, we’re going to be hearing a lot about the ‘fiscal cliff’: the threat that some 5% of GDP is going to be ripped out of the economy in a combination of tax hikes and spending cuts. A fiscal slow-down on that scale will almost certainly trigger recession. The CBO thinks so, though their numbers look optimistic to me. (If you cut demand by 5%, more or less overnight, then you shouldn’t expect the economy to grow by more than 1% in the year following.)

Because the process of fiscal compromise acts itself out on the political stage – all big personalities and high drama – the media loves to report it. Loves to imply that vast questions are at stake, that political careers will stand or fall by the outcome.

But they’re not. Not really. This so-called ‘cliff’ is really just the first in a series of steps. The US budget is arguably the most distorted in the Western world. Greece and Japan may have higher debts, Italy and Portugal may have worse growth prospects – but for sheer budgetary insanity, the US is probably the world leader, combining huge current deficits with vast unfunded promises to retirees, and welfare entitlement program recipients. You don’t need to take my word for this. The IMF states, ‘under our baseline scenario, a full elimination of the fiscal and generational imbalances would require all taxes to go up and all transfers to be cut immediately and permanently by 35 percent. A delay in the adjustment makes it more costly.’

The political ructions of the next few weeks will simply constitute the first scenes in a drama that will run for the next ten or fifteen years. And what’s more, this is a play where we already know the ending. Taxes will have to go up. Spending will have to come down. No other outcome is available: just ask the Greeks.

And meantime, there is a monetary time-bomb charged and ticking. A bomb which is being constantly primed with further explosive, further destructive force. Remember that the economic catastrophe of 2008 was created by loose monetary policy, the indisciplined expansion of credit and a market where increasingly shoddy securities were sold as investment grade assets. You might think that a logical reaction would be the steady tightening of policy and encouraging a climate of credit discipline.

Alas, however, such logic has no place at the Fed. Interest rates are on the floor, and have been for four years now. Because four years of loose money isn’t enough for the ivory-tower academics in charge of monetary policy, the Fed has explicitly committed to keep rates low indefinitely.

Loose money in the past, loose money guaranteed into the future … but that’s still not enough. The Fed has enlarged its balance sheet by $2 trillion since the crisis began to unfold. But that doesn’t even say it. The unelected officials at the Fed handed out an extraordinary $16 trillion in secret loans to bail out banks and businesses in the 2008-10 period. Those loans were not known to, or authorized by, Congress and many of the recipients were firms owned and headquarter abroad. Sen. Bernie Sanders, who has much to call attention to these issues, comments, ‘No agency of the United States government should be allowed to bailout a foreign bank or corporation without the direct approval of Congress and the president.’ Well, duh! It’s frankly extraordinary that there should be any question about this.

As Sanders also points out, the actual operation of the bailouts was largely outsourced in large part to investment banking firms on Wall Street who benefitted directly from the bailout. According to the Government Accountability Office, some two-thirds of such outsourcing contracts were awarded on a no-bid basis, an extraordinary failure. And meantime in a ‘money-laundering’ style operation, the Fed is acquiring $40 billion of low-quality mortgage backed securities – in many cases from the firms that created and missold them – thereby cleaning corrupt balance sheets at the risk of the US taxpayer.

The problems created by this unconstitutional misconduct go far beyond the mere trillions of dollars involved. The US Treasury market is being currently manipulated on a heroic scale. At times we’ve seen the Fed buying as much as 70% of US government bond issuance. Worse still, it’s effectively told the market that it intends to continue supporting the market as much as necessary for as long as necessary. In effect, we have a tiny group of unelected officials pursuing a set of radical and experimental policies – QE infinity, money-printing, unlimited bond buying, call it what you will.

And the theory behind this activity is simply crazy. When have price controls and state intervention ever worked? I don’t just mean for the US Treasuries market, but for any major market at any time? State intervention always fails. The Fed is simply setting up what looks set to be the largest Ponzi Scheme in history.

What’s more, because financial markets are interlinked, indiscipline in one market soon ripples through the system and unintended consequences impact many other markets. Wall Street traders, both currently and historically, price junk bonds off the US ten year treasury, which currently trades at an implausible 1.61%. But since the US Treasury market is flawed, every related market is too. As the Economist notes, a bubble is being inflated in government bonds, quality corporate bonds, junk bonds, and (I would add) global equities. As that newspaper comments, ‘When the market does turn everyone will want to head for the exit at once, as was the case with mortgage-related bonds in 2007. That might turn a retreat into a rout.’ I’d agree, except that the word might ought to be will.

And all this wouldn’t be so bad, except for one thing. What’s the exit strategy? Could it be hope-based by any chance? How do you climb down from these heights? Who will buy these bonds when the Fed stops? Who absorbs the losses? What exactly happens to the economy when interest rates normalize and bond prices collapse back to normal levels? Indeed, what happens to the banks when they can no longer sell their lousy assets to the Fed, can’t bump up their profits by selling no-bid services to the dumbest buyer in town? Too big to fail is still getting bigger.

The fiscal cliff is scary, because an abrupt one-off change in fiscal posture is a dumb way to do something that needs doing. But still, it needs doing. If a temporary economic slowdown is the price we pay for that, too bad. We’ll still be in better shape for taking the hit.

The monetary neutron bomb is worse. We’re still building it. No one’s talking about it. And the amounts are colossal.

“Geithner’s Treasury Department quietly warned at the end of October that the Treasury would reach current legal limit on the federal government’s debt by about the end of the year.”

By Elizabeth Harrington

November 19, 2012

(CNSNews.com) – Treasury Secretary Timothy Geithner said Friday that Congress should stop placing legal limits on the amount of money the government can borrow and effectively lift the debt limit to infinity.

On Bloomberg TV, “Political Capital” host Al Hunt asked Geithner if he believes “we ought to just eliminate the debt ceiling.”

“Oh, absolutely,” Geithner said.

One Trillion Dollars $1,000,000,000,000 The 2011 US federal deficit was $1.412 Trillion – 41% more than you see here. If you spent $1 million a day since Jesus was born, you would have not spent $1 trillion by now… but ~$700 billion-same amount the banks got during bailout. (click for sourcepage)

“You do? Will you propose that?” Hunt asked.

“Well, this is something only Congress can solve,” Geithner said. “Congress put it on itself. We’ve had 100 years of experience with it, and I think only once–last summer–did people decide to use it to threaten default on the American credit for the first time in history as a tool for political advantage. And that’s not a tenable strategy.”

Hunt then asked: “Is now the time to eliminate it?”

“It would have been time a long time ago to eliminate it,” Geithner said. “The sooner the better.”

Geithner’s Treasury Department quietly warned at the end of October that the Treasury would reach current legal limit on the federal government’s debt by about the end of the year.

In August 2011, President Barack Obama and Congress agreed to lift the legal debt limit by another $2.4 trillion–allowing the government to borrow up to $16.394 trillion. However, as of the close of business on Thursday, the Treasury had only $154.3 billion of that $2.4 trillion in new borrowing authority left.

Senate Majority Leader Harry Reid (D-Nev.) said last week that the Senate stands ready to increase the debt limit by another $2.4 trillion. “If it has to be raised, we’ll raise it,” Reid said.

$16.394 Trillion – 2012 US Debt Ceiling The US debt ceiling limit D-Day is estimated for September 14, 2012. US Debt has now surpassed the size of US economy in 2011– rated @ $15,064 Trillion. Statue of Liberty seems rather worried as United States national debt is soon to pass 20% of the entire world’s combined economy (GDP / Gross Domestic Product). “I predict future happiness for Americans if they can prevent the government from wasting the labors of the people under the pretense of taking care of them.” – Thomas Jefferson

“The political ructions of the next few weeks will simply constitute the first scenes in a drama that will run for the next ten or fifteen years. And what’s more, this is a play where we already know the ending. Taxes will have to go up. Spending will have to come down. No other outcome is available: just ask the Greeks.”

Over the coming weeks, we’re going to be hearing a lot about the ‘fiscal cliff’: the threat that some 5% of GDP is going to be ripped out of the economy in a combination of tax hikes and spending cuts. A fiscal slow-down on that scale will almost certainly trigger recession. The CBO thinks so, though their numbers look optimistic to me. (If you cut demand by 5%, more or less overnight, then you shouldn’t expect the economy to grow by more than 1% in the year following.)

Because the process of fiscal compromise acts itself out on the political stage – all big personalities and high drama – the media loves to report it. Loves to imply that vast questions are at stake, that political careers will stand or fall by the outcome.

But they’re not. Not really. This so-called ‘cliff’ is really just the first in a series of steps. The US budget is arguably the most distorted in the Western world. Greece and Japan may have higher debts, Italy and Portugal may have worse growth prospects – but for sheer budgetary insanity, the US is probably the world leader, combining huge current deficits with vast unfunded promises to retirees, and welfare entitlement program recipients. You don’t need to take my word for this. The IMF states, ‘under our baseline scenario, a full elimination of the fiscal and generational imbalances would require all taxes to go up and all transfers to be cut immediately and permanently by 35 percent. A delay in the adjustment makes it more costly.’

The political ructions of the next few weeks will simply constitute the first scenes in a drama that will run for the next ten or fifteen years. And what’s more, this is a play where we already know the ending. Taxes will have to go up. Spending will have to come down. No other outcome is available: just ask the Greeks.

And meantime, there is a monetary time-bomb charged and ticking. A bomb which is being constantly primed with further explosive, further destructive force. Remember that the economic catastrophe of 2008 was created by loose monetary policy, the indisciplined expansion of credit and a market where increasingly shoddy securities were sold as investment grade assets. You might think that a logical reaction would be the steady tightening of policy and encouraging a climate of credit discipline.

Alas, however, such logic has no place at the Fed. Interest rates are on the floor, and have been for four years now. Because four years of loose money isn’t enough for the ivory-tower academics in charge of monetary policy, the Fed has explicitly committed to keep rates low indefinitely.

Loose money in the past, loose money guaranteed into the future … but that’s still not enough. The Fed has enlarged its balance sheet by $2 trillion since the crisis began to unfold. But that doesn’t even say it. The unelected officials at the Fed handed out an extraordinary $16 trillion in secret loans to bail out banks and businesses in the 2008-10 period. Those loans were not known to, or authorized by, Congress and many of the recipients were firms owned and headquarter abroad. Sen. Bernie Sanders, who has much to call attention to these issues, comments, ‘No agency of the United States government should be allowed to bailout a foreign bank or corporation without the direct approval of Congress and the president.’ Well, duh! It’s frankly extraordinary that there should be any question about this.

As Sanders also points out, the actual operation of the bailouts was largely outsourced in large part to investment banking firms on Wall Street who benefitted directly from the bailout. According to the Government Accountability Office, some two-thirds of such outsourcing contracts were awarded on a no-bid basis, an extraordinary failure. And meantime in a ‘money-laundering’ style operation, the Fed is acquiring $40 billion of low-quality mortgage backed securities – in many cases from the firms that created and missold them – thereby cleaning corrupt balance sheets at the risk of the US taxpayer.

The problems created by this unconstitutional misconduct go far beyond the mere trillions of dollars involved. The US Treasury market is being currently manipulated on a heroic scale. At times we’ve seen the Fed buying as much as 70% of US government bond issuance. Worse still, it’s effectively told the market that it intends to continue supporting the market as much as necessary for as long as necessary. In effect, we have a tiny group of unelected officials pursuing a set of radical and experimental policies – QE infinity, money-printing, unlimited bond buying, call it what you will.

And the theory behind this activity is simply crazy. When have price controls and state intervention ever worked? I don’t just mean for the US Treasuries market, but for any major market at any time? State intervention always fails. The Fed is simply setting up what looks set to be the largest Ponzi Scheme in history.

What’s more, because financial markets are interlinked, indiscipline in one market soon ripples through the system and unintended consequences impact many other markets. Wall Street traders, both currently and historically, price junk bonds off the US ten year treasury, which currently trades at an implausible 1.61%. But since the US Treasury market is flawed, every related market is too. As the Economist notes, a bubble is being inflated in government bonds, quality corporate bonds, junk bonds, and (I would add) global equities. As that newspaper comments, ‘When the market does turn everyone will want to head for the exit at once, as was the case with mortgage-related bonds in 2007. That might turn a retreat into a rout.’ I’d agree, except that the word might ought to be will.

And all this wouldn’t be so bad, except for one thing. What’s the exit strategy? Could it be hope-based by any chance? How do you climb down from these heights? Who will buy these bonds when the Fed stops? Who absorbs the losses? What exactly happens to the economy when interest rates normalize and bond prices collapse back to normal levels? Indeed, what happens to the banks when they can no longer sell their lousy assets to the Fed, can’t bump up their profits by selling no-bid services to the dumbest buyer in town? Too big to fail is still getting bigger.

The fiscal cliff is scary, because an abrupt one-off change in fiscal posture is a dumb way to do something that needs doing. But still, it needs doing. If a temporary economic slowdown is the price we pay for that, too bad. We’ll still be in better shape for taking the hit.

The monetary neutron bomb is worse. We’re still building it. No one’s talking about it. And the amounts are colossal.